There's a persistent myth in options trading that selling premium requires watching screens all day — stalking IV ticks, refreshing chains, reacting to every intraday spike. It doesn't. The best premium-selling setups aren't found in real-time noise; they're found in the data that accumulates after the market closes.

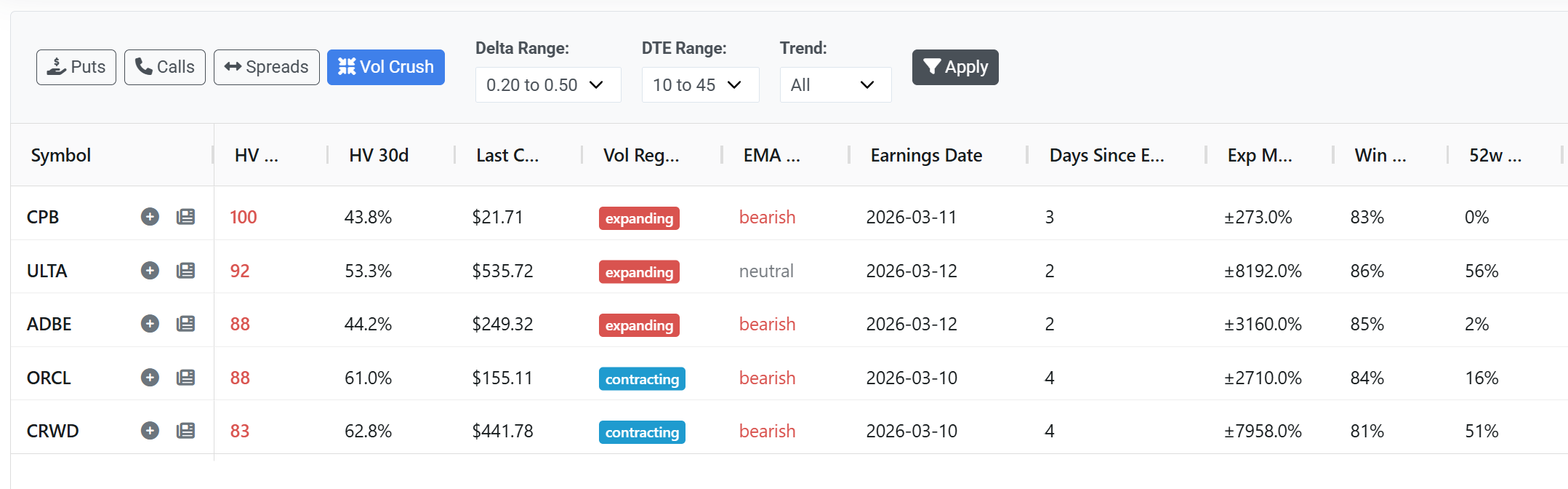

Tiblio's new Vol Crush Screener runs nightly across the entire S&P 500, pricing every tradeable option using pure historical volatility and ranking each stock against 52 weeks of its own vol history. No implied volatility circularity, no chasing intraday phantoms, just a clean read on where premium is genuinely rich.

But knowing vol is elevated is only half the picture. The screener layers in earnings proximity, SEC insider filings, analyst actions, trend confirmation, and a walk-forward test that shows you the actual historical win rate of each setup.

Every opportunity gets scored, risk-flagged, and structured — naked or spread — so you wake up to a ranked list of trades that have already been vetted by the signals that matter. No gut calls, no FOMO entries, no discovering after the fact that insiders were dumping shares the whole time.

The feature we're most excited about: Vol Crush opportunities. Most traders think vol crush is strictly an earnings play — sell before the event, collect the IV collapse. But elevated volatility doesn't always disappear the moment earnings pass. Our scanner catches the window where HV rank is still running hot while implied vol starts to compress, handing you time decay and volatility decay working together.

New historical vol data, signals, and the full screener are coming soon — stay tuned.